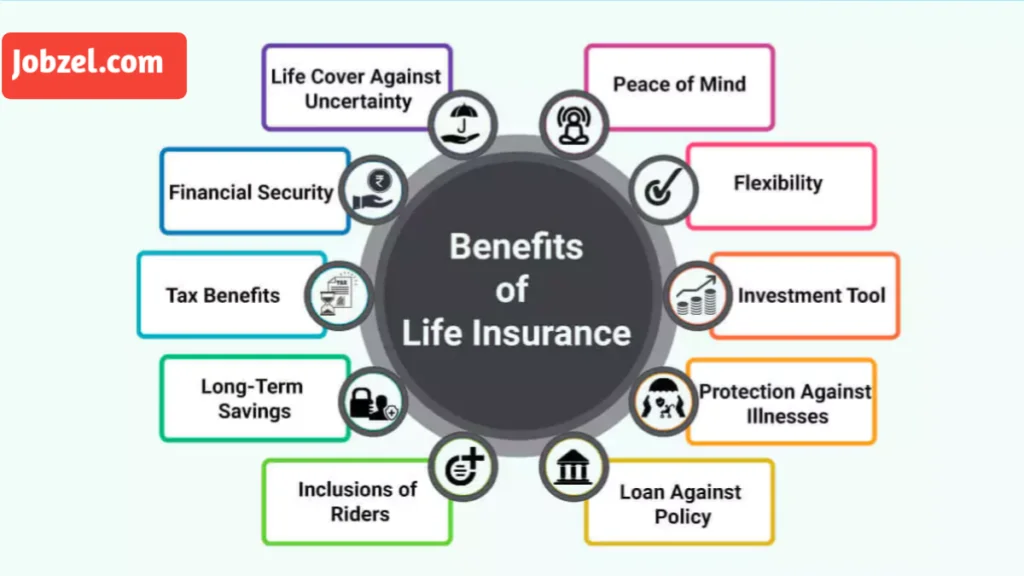

Introduction:

Life insurance is often viewed as a safety net, a financial cushion for loved ones in the event of an untimely death. But what if we told you that life insurance could be so much more? Beyond the basic payout, life insurance policies can be powerful tools for wealth accumulation, tax planning, and even retirement savings. In this comprehensive guide, we’ll explore how to maximize your life insurance benefits, ensuring that you and your family are not only protected but also financially empowered. Whether you’re a young professional just starting to think about the future or a seasoned investor looking to optimize your portfolio, this guide will provide you with actionable strategies to make the most of your life insurance policy.

Section 1: Understanding the Different Types of Life Insurance Policies

Before diving into strategies for maximizing your life insurance benefits, it’s crucial to understand the different types of policies available. The two primary categories are term life insurance and permanent life insurance.

- Term Life Insurance: This is the most straightforward and affordable option. It provides coverage for a specific period, typically 10, 20, or 30 years. If the policyholder passes away during the term, the beneficiaries receive a death benefit. However, if the term expires and the policyholder is still alive, there’s no payout. Term life is ideal for those who need coverage for a specific period, such as until their children are financially independent or a mortgage is paid off.

- Permanent Life Insurance: This category includes whole life, universal life, and variable life insurance. Unlike term life, permanent life insurance provides lifelong coverage and includes a cash value component that grows over time. This cash value can be borrowed against or withdrawn, offering a unique financial tool for policyholders. Permanent life insurance is more expensive but offers long-term benefits that go beyond just a death benefit.

Understanding these options is the first step in choosing the right policy for your needs. Each type has its pros and cons, and the best choice depends on your financial goals, age, and risk tolerance.

Section 2: Leveraging the Cash Value Component of Permanent Life Insurance

One of the most underutilized features of permanent life insurance is the cash value component. This feature allows policyholders to build wealth over time, offering a unique combination of protection and investment.

- How It Works: A portion of your premium payments goes into a cash value account, which grows tax-deferred over time. The growth rate depends on the type of policy you have. For example, whole life insurance offers a guaranteed growth rate, while variable life insurance allows you to invest in sub-accounts similar to mutual funds.

- Borrowing Against Your Policy: One of the key benefits of the cash value is the ability to borrow against it. These loans are typically tax-free and don’t require a credit check, making them an attractive option for funding major expenses like college tuition, home renovations, or even starting a business. However, it’s important to repay the loan to avoid reducing the death benefit.

- Tax Advantages: The cash value grows tax-deferred, meaning you won’t pay taxes on the gains until you withdraw them. Additionally, if structured correctly, the death benefit is generally tax-free for your beneficiaries.

By understanding and leveraging the cash value component, you can turn your life insurance policy into a powerful financial tool that provides both protection and growth opportunities.

Section 3: Using Life Insurance for Estate Planning and Tax Efficiency

Life insurance isn’t just about providing for your loved ones after you’re gone; it can also play a crucial role in estate planning and tax efficiency.

- Estate Planning: For high-net-worth individuals, life insurance can be used to cover estate taxes, ensuring that your heirs receive the full value of your estate without having to sell off assets. By setting up an irrevocable life insurance trust (ILIT), you can remove the death benefit from your taxable estate, further reducing the tax burden on your beneficiaries.

- Tax Efficiency: Life insurance offers several tax advantages. As mentioned earlier, the cash value grows tax-deferred, and the death benefit is generally tax-free. Additionally, if you’re using life insurance as part of a charitable giving strategy, you can receive tax deductions while supporting a cause you care about.

- Business Succession Planning: If you own a business, life insurance can be used to fund a buy-sell agreement, ensuring a smooth transition of ownership in the event of your death. This can prevent disputes among heirs and provide liquidity to the business.

By incorporating life insurance into your estate plan, you can protect your assets, minimize taxes, and ensure that your legacy is preserved for future generations.

Section 4: Life Insurance as a Retirement Planning Tool

While most people think of life insurance as a tool for protecting their family, it can also be an effective retirement planning tool, especially for those who have maxed out other retirement accounts like 401(k)s and IRAs.

- Supplementing Retirement Income: The cash value in a permanent life insurance policy can be accessed during retirement, providing a source of tax-advantaged income. Unlike withdrawals from a traditional IRA or 401(k), which are taxed as ordinary income, withdrawals from the cash value are generally tax-free up to the amount of premiums paid.

- Long-Term Care Benefits: Some life insurance policies offer long-term care riders, which allow you to use the death benefit to cover long-term care expenses. This can be a valuable feature, as long-term care costs can quickly deplete retirement savings.

- Legacy Planning: If you don’t need the cash value for retirement, it can be left to grow and passed on to your beneficiaries as part of your legacy. This can provide a significant financial boost to your heirs, especially if you’ve already used other retirement accounts to fund your retirement.

By integrating life insurance into your retirement plan, you can create a more secure and flexible financial future.

Section 5: Common Mistakes to Avoid When Maximizing Life Insurance Benefits

While life insurance offers numerous benefits, there are also pitfalls to avoid. Here are some common mistakes that can undermine your efforts to maximize your policy’s potential:

- Underinsuring: One of the biggest mistakes is not having enough coverage. Many people underestimate the amount of life insurance they need, leaving their loved ones financially vulnerable. A good rule of thumb is to have coverage that’s 10-15 times your annual income.

- Overlooking Policy Riders: Policy riders can add valuable features to your life insurance policy, such as accelerated death benefits, waiver of premium, or long-term care coverage. However, many people overlook these options, missing out on additional benefits.

- Failing to Review Your Policy: Life insurance needs change over time. What was appropriate when you were 30 may not be sufficient when you’re 50. Regularly reviewing your policy ensures that it continues to meet your needs.

- Borrowing Too Much Against Cash Value: While borrowing against your policy can be a useful tool, overborrowing can reduce the death benefit and potentially cause the policy to lapse. It’s important to manage loans carefully and repay them as soon as possible.

By avoiding these common mistakes, you can ensure that your life insurance policy provides the maximum benefit for you and your loved ones.

Conclusion:

Life insurance is more than just a safety net; it’s a versatile financial tool that can provide protection, growth, and tax advantages. By understanding the different types of policies, leveraging the cash value component, and incorporating life insurance into your estate and retirement plans, you can maximize the benefits of your policy and secure your financial future. Whether you’re looking to protect your family, build wealth, or plan for retirement, life insurance offers a range of options to meet your needs. Take the time to review your policy, explore additional features, and consult with a financial advisor to ensure that you’re making the most of your life insurance benefits. Your future self—and your loved ones—will thank you.

![]()