For business owners, building a successful enterprise is just the first chapter of their legacy story. The more challenging task often lies in ensuring that the wealth and business they’ve created continues to thrive for generations to come. With complex tax laws, family dynamics, and business succession planning to consider, comprehensive estate planning becomes not just important—it becomes essential.

The Hidden Complexities of Business Estate Planning

Most successful business owners understand the basics of estate planning—wills, trusts, and power of attorney documents. However, when a business is involved, the stakes are dramatically higher, and the planning process becomes significantly more intricate. Consider this: according to the Family Business Institute, only about 30% of family businesses survive into the second generation, and merely 12% make it to the third. These sobering statistics often stem from inadequate estate planning.

The challenge isn’t just about passing on assets; it’s about ensuring business continuity, minimizing tax exposure, and maintaining family harmony. For business owners, proper estate planning can mean the difference between their life’s work continuing to thrive or facing dissolution due to preventable circumstances.

Essential Components of a Business Owner’s Estate Plan

Business Succession Planning

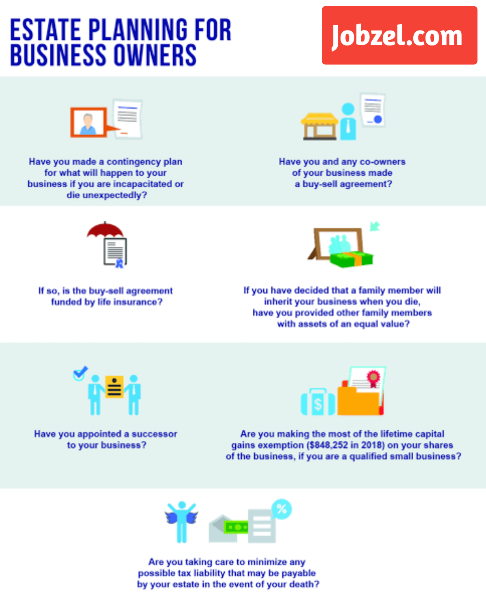

Creating a comprehensive succession plan is perhaps the most critical element of estate planning for business owners. This involves more than simply naming who will take over—it requires detailed consideration of multiple factors:

- Leadership transition timeline and strategy

- Training and development plans for successors

- Contingency plans for unexpected events

- Business valuation and transfer mechanisms

- Key employee retention strategies

A well-structured succession plan should address both planned transitions and unexpected scenarios. For instance, if you become incapacitated, who has the authority to make immediate business decisions? How will ownership transfers be funded? These questions need clear answers before they become urgent issues.

Tax Minimization Strategies

Estate tax considerations for business owners are particularly complex, as they must navigate both personal and business tax implications. Several strategies can help minimize tax exposure:

- Family Limited Partnerships (FLPs)

- Allow for gradual transfer of business ownership

- Provide significant tax advantages through valuation discounts

- Maintain senior generation control while transferring economic benefits

- Grantor Retained Annuity Trusts (GRATs)

- Enable tax-efficient transfer of appreciating business interests

- Provide income stream to business owner during trust term

- Reduce gift tax exposure on transfers to next generation

- Buy-Sell Agreements

- Establish clear ownership transition plans

- Provide funding mechanism for ownership transfers

- Help establish business value for estate tax purposes

Advanced Planning Techniques for Business Protection

Case Study: The Smith Family Manufacturing Company

Consider the case of John Smith, owner of a successful manufacturing company valued at $15 million. John implemented a comprehensive estate plan that included:

- Creating an irrevocable life insurance trust (ILIT) to provide liquidity for estate taxes

- Establishing a family limited partnership to facilitate gradual ownership transfer

- Implementing a qualified personal residence trust (QPRT) for his primary residence

- Setting up a charitable remainder trust (CRT) for tax-efficient philanthropic giving

The result? When John passed away unexpectedly, his business continued operating smoothly, his family avoided forced asset sales to pay estate taxes, and his charitable legacy was secured.

Asset Protection Strategies

In today’s litigious environment, protecting business assets becomes crucial. Consider implementing:

Legal Entity Structuring

- Separate operating entities from asset-holding entities

- Use holding companies for intellectual property

- Establish multiple operating entities to isolate risks

Insurance Coverage

- Key person insurance

- Buy-sell funding insurance

- Umbrella liability coverage

- Professional liability protection

Family Dynamics and Communication Planning

One often-overlooked aspect of business estate planning is managing family expectations and communication. Statistics show that family conflicts, rather than business or tax issues, are often the primary cause of failed succession plans.

Best Practices for Family Business Communication:

- Regular family meetings to discuss business matters

- Clear documentation of roles and responsibilities

- Professional mediation for conflict resolution

- Written policies for family member involvement

- Transparent compensation and promotion criteria

Digital Asset Considerations

In today’s digital age, business owners must also plan for their digital assets:

- Online banking and financial accounts

- Social media accounts and online presence

- Customer databases and digital records

- Intellectual property and digital assets

- Cryptocurrency and digital investments

Creating Your Estate Planning Strategy

The process of creating a comprehensive estate plan should involve several key professionals:

- Estate planning attorney

- Business succession planner

- Tax advisor or CPA

- Financial planner

- Insurance specialist

Working with this team of professionals ensures that all aspects of your estate plan are properly coordinated and aligned with your objectives.

Conclusion: Taking Action to Protect Your Legacy

Estate planning for business owners is a complex but crucial process that requires careful consideration and regular review. The consequences of inadequate planning can be severe, potentially leading to business failure, family conflicts, and unnecessary tax burdens.

Don’t wait for a crisis to begin planning. Start by assembling your team of professional advisors and conducting a thorough review of your current situation. Consider how your business has evolved, how your family dynamics have changed, and what new opportunities or challenges have emerged in the tax and legal landscape.

Ready to take the next step in protecting your business legacy? Schedule a consultation with an experienced estate planning attorney who specializes in business succession planning. Your family’s future and your business’s legacy are too important to leave to chance.

![]()